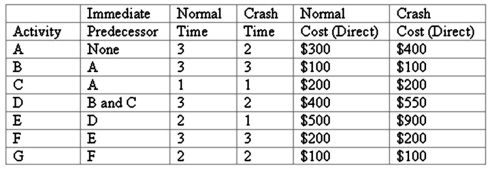

You have collected the data for a time-cost CPM scheduling model analysis.The time is in days and the project "direct costs" are given here.  The indirect costs for the project are determined on a daily duration basis.If the project lasts 16 days, the total indirect costs are $400; 15 days, they will be $250; 14 days, they will be $200; and 13 days, they will be $100.If you crash this project by one day what is the total (i.e., direct and indirect) project cost? ____________________

The indirect costs for the project are determined on a daily duration basis.If the project lasts 16 days, the total indirect costs are $400; 15 days, they will be $250; 14 days, they will be $200; and 13 days, they will be $100.If you crash this project by one day what is the total (i.e., direct and indirect) project cost? ____________________

E.A costs $100/day to crash, D costs $150/day to crash, and E costs $400/day to crash.Reducing the duration of A by one day at an additional cost of $100 is the most economical.Direct costs are now $400 + $100 + $200 + $400 + $500 + $200 + $100 = $1,900.Overall duration of the project is 15 days, and indirect costs are $250.The total cost of crashing this project for one day is $2,150.

Definitions:

Total Consumer Surplus

The total benefit received by consumers in a market transaction, measured as the difference between what consumers are willing to pay and what they actually pay.

Price Ceiling

A government-imposed limit on how high the price of a good or service can be charged, usually intended to protect consumers.

Consumer Surplus

The difference between what consumers are willing to pay for a good or service and what they actually pay.

Producer Surplus

The difference between what producers are willing to accept for a good or service versus what they actually receive, typically illustrated as the area above the supply curve and below the market price.

Q2: Using attraction-selection-attrition (ASA) theory, describe how a

Q8: Which of the following is a characteristic

Q8: Explain the six strategies for reducing restraining

Q12: Mechanistic structures are better suited to dynamic

Q25: Which of the following is not a

Q54: Unfreezing occurs when the driving forces are

Q56: One of the assumptions made using CPM

Q74: Appreciative inquiry tries to break away from

Q103: Companies can be centralized in some parts

Q110: Outline the action research approach to organizational