On December 31,20X1,Dad Ltd.purchased 100% of the outstanding common shares of the Sad Ltd.for $9.5 million in cash.On that date,the shareholders' equity of Sad totaled $8 million and consisted of $1 million in no par common shares and $7 million in retained earnings.Both companies use the straight-line method to calculate depreciation.Goodwill,if any arises as a result of this business combination,is written down when there is impairment.Both Dad and Sad report under accounting standards for private enterprises.

For the year ending December 31,20X6,the statements of earnings for Dad and Sad were as follows:

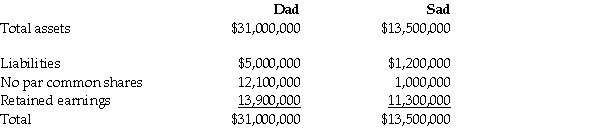

As at December 31,20X6,the condensed statements of financial position for the two companies were as follows:

OTHER INFORMATION:

1.On December 31,20X1,Sad had a building with a fair value that was $300,000 greater than its carrying value.The building had an estimated remaining useful life of 20 years.

2.On December 31,20X1,Sad had inventory with a fair value that was $200,000 less than its carrying value.This inventory was sold in 20X3.

3.During 20X6,Dad sold merchandise to Sad for $100,000,a price that includes a gross profit of $40,000.During 20X6,40% of this merchandise was resold by Sad to third parties and the other 60% remains in its December 31,20X6 inventories.On December 31,20X5,the inventories of Sad contained merchandise purchased from Dad on which Dad had recognized a gross profit in the amount of $20,000.

4.During 20X6,Dad declared and paid dividends of $300,000 while Sad declared and paid dividends of $100,000.

5.Dad accounts for its investment in Sad using the cost method.

6.The retained earnings of Dad as at December 31,20x5 was $12,000,000.On that date,Sad had retained earnings of $9,800,000.Sad has not issued any common shares since its acquisition by Dad.

7.There were no specific events or circumstances between 20X2 and 20X6 to indicate any impairment of goodwill.

Required:

Calculate consolidated net income for the year ending December 31,20X6.

Definitions:

Roediger-McDermott Paradigm

A cognitive psychology experiment that demonstrates the creation of false memories through the presentation of lists of semantically related words.

False Recall

A psychological phenomenon where individuals remember events or details that never occurred.

Psychoanalytic Tradition

A framework in psychology, originated by Sigmund Freud, which emphasizes the role of unconscious factors in personality and behavior.

Repress Memories

The psychological defense mechanism where an individual unconsciously blocks out memories that are too traumatic or stressful to confront.

Q11: Under the direct method,what values should be

Q19: Which of the following is not an

Q26: Cho Co. ,a public Canadian corporation has

Q27: Under IFRS,which of the following statements is

Q35: O'Reilly Ltd.incorporated O'Reilly R&D Co.to conduct research

Q55: owners of Old School Brand Authentic Antique

Q70: Franconia Sales offers warranties on all

Q119: internal response that customers have to all

Q129: On January 2,2014,Mahoney Sales issued $10,000 in

Q157: Which of the following is an important