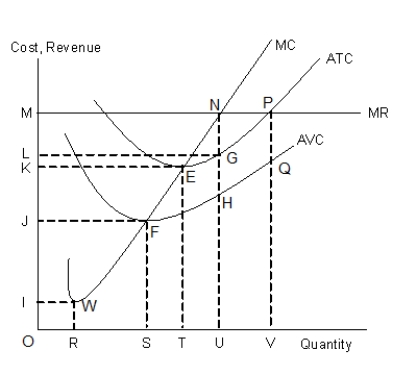

The figure given below shows the revenue and cost curves of a perfectly competitive firm.Figure 10.1

-Suppose that in a perfectly competitive market, the market supply of a good increases. As a result, the individual firm's:

Definitions:

Monopolist

An individual or company that holds exclusive control over the supply or trade of a particular good or service, allowing them to influence prices and market conditions.

Short-Run

The short-run in economics refers to a period during which at least one input, such as plant size, is fixed and cannot be changed.

Long-Run

A period of time in which all factors of production and costs are variable, allowing for full adjustment to changes.

Marginal Revenue

The increase in revenue from the sale of one more unit of a product or service.

Q2: When consumers have perfect information about the

Q9: In Figure 10.3, at equilibrium, the firm

Q27: Refer to Table 8.2. If the production

Q30: Fixed costs are costs paid for:<br>A)medical reimbursements

Q42: What is the total social surplus prior

Q43: The difference between average total cost and

Q54: If one were to plot the data

Q77: Which of the following reflects the correct

Q101: If a 10 percent increase in price

Q130: Given the above equation, the quantity of