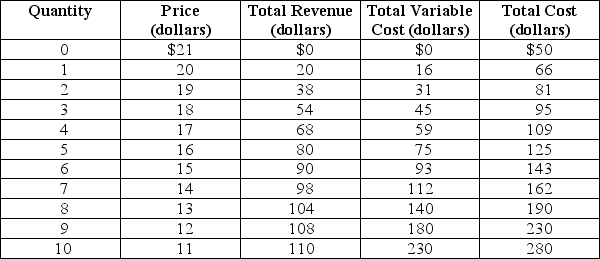

Table 13-3

Table 13-3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 13-3.What is its average variable cost of production at its optimal output level?

Definitions:

Income

Earnings acquired, frequently on a steady basis, through employment or investing activities.

Consumer Equilibrium

The point at which the quantity of goods and services a consumer chooses to buy equates to the maximum satisfaction or utility for their budget.

Budget Constraint

The limitation on the consumption bundles that a consumer can afford based on their income and the prices of goods.

Consumer Equilibrium

The point at which an individual's income is perfectly balanced with their consumption preferences, maximizing utility.

Q9: In the real world,<br>A) all sellers charge

Q15: If,for the last unit of a good

Q24: Refer to Figure 13-11.The diagram demonstrates that<br>A)

Q52: For a natural monopoly to exist,<br>A) a

Q73: Which of the following costs will not

Q74: If an industry is made up of

Q75: Which of the following products allows the

Q116: A firm that successfully differentiates its product

Q118: Refer to Table 14-4.Suppose the payoff matrix

Q130: Refer to Figure 15-9.Why won't regulators require