You have collected quarterly data on Canadian unemployment (UrateC)and inflation (InfC)from 1962 to 1999 with the aim to forecast Canadian inflation.

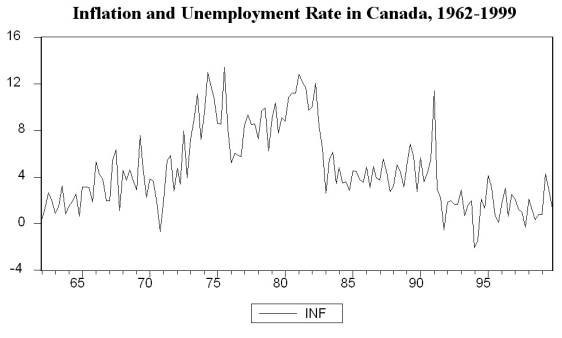

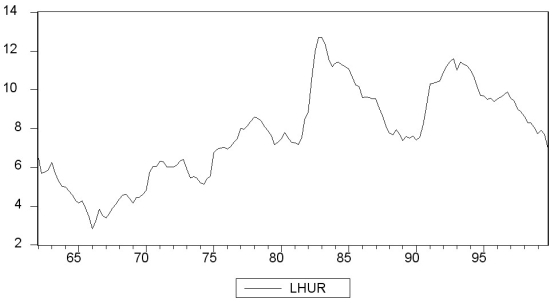

(a)To get a better feel for the data,you first inspect the plots for the series.

Inspecting the Canadian inflation rate plot and having calculated the first autocorrelation to be 0.79 for the sample period,do you suspect that the Canadian inflation rate has a stochastic trend? What more formal methods do you have available to test for a unit root?

Inspecting the Canadian inflation rate plot and having calculated the first autocorrelation to be 0.79 for the sample period,do you suspect that the Canadian inflation rate has a stochastic trend? What more formal methods do you have available to test for a unit root?

(b)You run the following regression,where the numbers in parenthesis are homoskedasticity-only standard errors:  = 0.49- 0.10 Inft-1 - 0.39 △InfCt-1 - 0.33 △InfCt-2 - 0.21 △InfCt-3 + 0.05 △InfCt-4

= 0.49- 0.10 Inft-1 - 0.39 △InfCt-1 - 0.33 △InfCt-2 - 0.21 △InfCt-3 + 0.05 △InfCt-4

(0.28)(0.05)(0.09)(0.09)(0.09)(0.08)

Test for the presence of a stochastic trend.Should you have used heteroskedasticity-robust standard errors? Does the fact that you use quarterly data suggest including four lags in the above regression,or how should you determine the number of lags?

(c)To forecast the Canadian inflation rate for 2000:I,you estimate an AR(1),AR(4),and an ADL(4,1)model for the sample period 1962:I to 1999:IV.The results are as follows:  = 0.002 - 0.31 △InfCt-1

= 0.002 - 0.31 △InfCt-1

(0.014)(0.10)  = 0.021 - 0.46 ΔInfCt-1 - 0.39 ΔInfCt-2 - 0.25 ΔInfCt-3 + 0.03 ΔInfCt-4

= 0.021 - 0.46 ΔInfCt-1 - 0.39 ΔInfCt-2 - 0.25 ΔInfCt-3 + 0.03 ΔInfCt-4

(0.158)(0.10)(0.11)(0.08)(0.07)  = 1.279 - 0.51 ΔInfCt-1 - 0.44 ΔInfCt-2 - 0.30 ΔInfCt-3 - 0.02 ΔInfCt-4

= 1.279 - 0.51 ΔInfCt-1 - 0.44 ΔInfCt-2 - 0.30 ΔInfCt-3 - 0.02 ΔInfCt-4

(0.57)(0.10)(0.11)(0.09)(0.08)

- 0.16 UrateCt-1

(0.07)

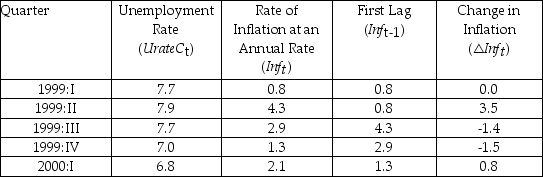

In addition,you have the following information on inflation in Canada during the four quarters of 1999 and the first quarter of 2000:

Inflation and Unemployment in Canada,First Quarter 1999 to First Quarter 2000

For each of the three models,calculate the predicted inflation rate for the period 2000:I and the forecast error.

For each of the three models,calculate the predicted inflation rate for the period 2000:I and the forecast error.

(d)Perform a test on whether or not Canadian unemployment rates Granger-cause the Canadian inflation rate.

Definitions:

Excretion

The process by which metabolic waste products are eliminated from an organism to maintain homeostasis.

Immunity

The ability of an organism to resist and fight off infections and diseases through the action of specific antibodies or sensitized white blood cells.

Arterioles

Small blood vessels that extend and branch out from arteries, leading to capillaries; they play a key role in regulating blood pressure.

Dermal Blood Vessels

Refers to the network of blood vessels situated within the dermal layer of the skin, which provide nutrients and regulate temperature.

Q18: The textbook formula for the variance of

Q19: Using the California School data set from

Q26: The probit model<br>A)is the same as the

Q38: The probability of an outcome<br>A)is the number

Q41: It is advisable to use clustered standard

Q41: You have a limited dependent variable (Y)and

Q47: Consider the following regression line: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB2833/.jpg"

Q52: Your textbook extends the simple regression analysis

Q69: The textbook mentioned that the mean of

Q115: An agency responsible for coordinating organ donations