Jakeman Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead.

The standard cost card for the company's only product is as follows:

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $351,000 and budgeted activity of 27,000 hours.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $351,000 and budgeted activity of 27,000 hours.

During the year, the company completed the following transactions:

a. Purchased 76,600 gallons of raw material at a price of $7.90 per gallon.

b. Used 70,960 gallons of the raw material to produce 20,900 units of work in process.

c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 18,710 hours at an average cost of $19.40 per hour.

d. Applied fixed overhead to the 20,900 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $334,600. Of this total, $252,600 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $82,000 related to depreciation of manufacturing equipment.

e. Completed and transferred 20,900 units from work in process to finished goods.

f. Sold (for cash) 17,700 units to customers at a price of $74.30 per unit.

g. Transferred the standard cost associated with the 17,700 units sold from finished goods to cost of goods sold.

h. Paid $93,000 of selling and administrative expenses.

i. Closed all standard cost variances to cost of goods sold.

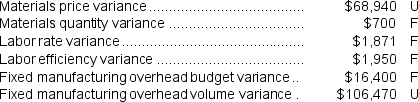

The company calculated the following variances for the year:

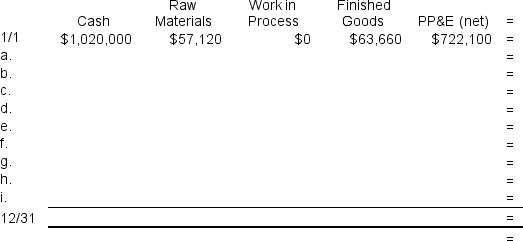

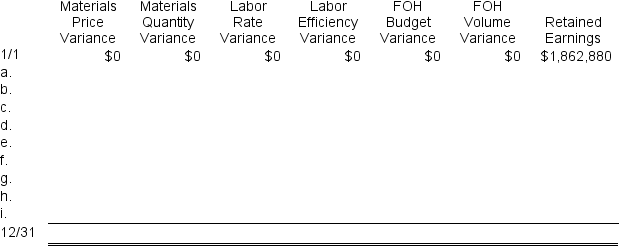

To answer the following questions, it would be advisable to record transactions a through i in the worksheet below. This worksheet is similar to the worksheets in your text except that it has been split into two parts to fit on the page. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

To answer the following questions, it would be advisable to record transactions a through i in the worksheet below. This worksheet is similar to the worksheets in your text except that it has been split into two parts to fit on the page. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

-The adjusted Cost of Goods Sold after closing all of the variances to Cost of Goods Sold will be closest to:

Definitions:

Street Vendors

Individuals who sell goods or food in public places, often from a cart, table, or small stall.

Market Town

A town that traditionally holds markets, providing a trading venue for the people in the surrounding area.

Substantive Due Process

A constitutional principle that protects individuals from the government's infringement on fundamental constitutional liberties.

Kentucky State Statute

Laws enacted by the Kentucky state legislature that govern legal obligations and rights within the state of Kentucky.

Q18: For performance evaluation purposes,how much of the

Q26: When a dispute arises over a transfer

Q74: The fixed manufacturing overhead volume variance for

Q82: The predetermined overhead rate is closest to:<br>A)

Q98: The direct materials in the flexible budget

Q103: The net operating income for the year

Q143: Duboise Corporation makes a product with the

Q143: The amount shown for "Other expenses" in

Q153: The division's residual income is closest to:<br>A)

Q219: The labor efficiency variance for July is:<br>A)