Figure 35-7

Use the two graphs in the diagram to answer the following questions.

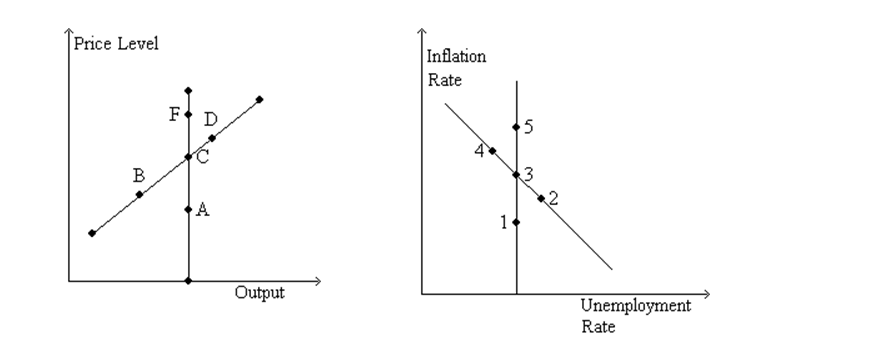

-Refer to Figure 35-7.The economy would move from 3 to 5

Definitions:

Competitive Increasing-cost Industry

An industry in which the entry of new firms causes the prices of inputs to increase, affecting the cost of production for all firms.

Long-run Equilibrium

A state in which all factors of production and inputs can be varied, allowing for full adjustment by firms and the economy, and no excess demand or supply exists.

Decline in Demand

A decrease in the willingness and ability of consumers to buy goods and services at existing prices, which can lead to lower market prices.

Constant-cost Industry

An industry in which the costs of production, including inputs and labor, do not change as the overall industry output changes.

Q2: Refer to Figure 35-3.What is measured along

Q3: According to traditional Keynesian analysis,if the economy

Q4: If people decide to hold less money,then<br>A)money

Q8: The demand for a good or service

Q20: If the sacrifice ratio is 2,reducing the

Q31: Suppose that money supply growth increases.In the

Q33: Which of the following is not an

Q37: The lag problem associated with monetary policy

Q73: Which of the following would reduce the

Q99: According to the long-run Phillips curve,in the