Consider the model Yi - β1Xi + ui,where the Xi and ui the are mutually independent i.i.d.random variables with finite fourth moment and E(ui)= 0.

(a)Let  1 denote the OLS estimator of β1.Show that

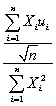

1 denote the OLS estimator of β1.Show that  (

(  1- β1)=

1- β1)=  .

.

(b)What is the mean and the variance of  ? Assuming that the Central Limit Theorem holds,what is its limiting distribution?

? Assuming that the Central Limit Theorem holds,what is its limiting distribution?

(c)Deduce the limiting distribution of  (

(  1 - β1)? State what theorems are necessary for your deduction.

1 - β1)? State what theorems are necessary for your deduction.

Definitions:

Agents

Individuals or entities authorized to act on behalf of another person or entity in business transactions or legal matters.

Commodities Market

A marketplace where traders buy and sell raw physical products such as gold, oil, or agricultural products.

Ownership

The legal right or status of having control over property, resources, or assets.

Wheat

A cereal grain that is a staple food used to make flour for bread, pasta, pastry, and other food products.

Q4: Consider a typical beta convergence regression function

Q7: When you add state fixed effects to

Q30: Explain carefully why testing joint hypotheses simultaneously,using

Q40: The OLS residuals in the multiple regression

Q41: The IV estimator can be used to

Q42: An agency responsible for coordinating organ donations

Q46: Time series variables fail to be stationary

Q95: A particular paperback mystery book is published

Q101: Even though Puerto Rico is a commonwealth

Q110: There was a wonderful study conducted in